South Africans are once again being targeted by these sophisticated scammers posing as SARS, however this instance is particularly dangerous as it mirrors the reality of South Africa’s current tax environment, where taxpayers are being increasingly contacted by SARS, who are committed to recovering legitimate tax liabilities.

Discerning between legitimate communication from SARS and scam attempts are crucial, especially where communications appear to be legitimate, the wording appears formal, and references to legal enforcement resemble the type of communication many taxpayers increasingly expect from SARS itself.

SARS Modernisation 3.0 Has Changed the Landscape

The emergence of these scams are not coincidental, as with SARS’ Modernisation 3.0 strategy, SARS has significantly strengthened its enforcement and collection capabilities. Enhanced data analytics, third party data matching, artificial intelligence driven verification systems, and improved banking integration have materially increased SARS’ visibility into taxpayer affairs.

This results in a more assertive collection environment, where outstanding returns, unpaid taxes, verification audits, penalties, and debt collection processes are becoming increasingly common experiences for taxpayers and businesses alike.

SARS have made revenue collection a clear strategic priority as pressure on the fiscus continues to intensify. The problem that accompanies this, is that scammers recognise the opportunity for crime that this creates.

Scammers understand that many taxpayers are already anxious about unresolved compliance issues or outstanding liabilities. A fake “settlement notification” therefore becomes far more believable in an environment where SARS itself is taking a stronger approach to enforcement.

The Importance of Verification

The greatest danger with these scams is that they rely on emotional decision making. Taxpayers who receive threatening correspondence referencing legal action or “immediate” payment demands may react before properly verifying the communication. In many cases, fear unfortunately overrides caution.

At the same time, some taxpayers have become so accustomed to scam communications that they now ignore legitimate SARS notices altogether, creating a separate compliance risk entirely. Every SARS communication should therefore be treated seriously but independently verified before any action is taken.

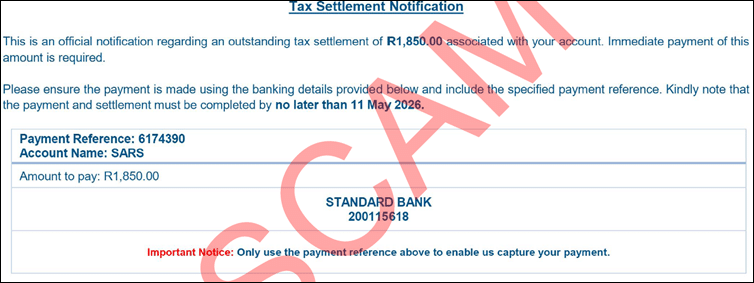

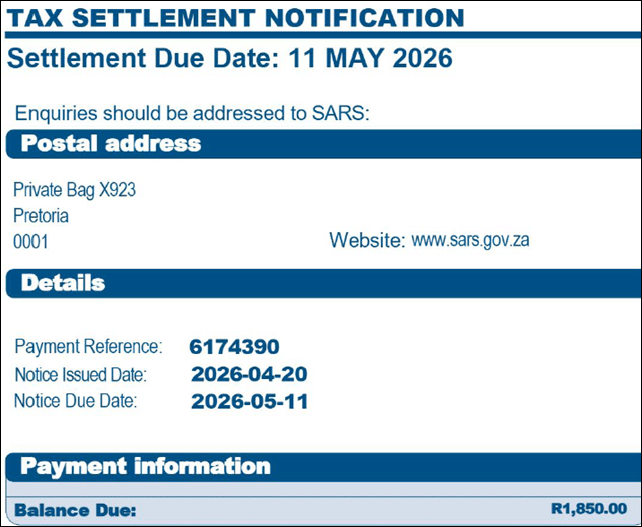

Scam communications often contain warning signs such as suspicious links, unofficial payment channels, urgent or immediate payment deadlines, requests for banking information, or email domains designed to imitate SARS branding.

Crucially however, these communications do not contain actual taxpayer information, such as a tax reference number, ID numbers, or even taxpayer names which are always reflected on legitimate communications:

SARS has repeatedly confirmed that taxpayers should verify all correspondence through official platforms such as SARS eFiling, or directly with recognised SARS officials and tax practitioners.

For the more perceptive taxpayer, the wording of these communications do indicate possible fraud, including but not limited to grammatical errors, spelling errors, and incorrect citations of law, such as section 95(1)(a), which does not relate to collection measures, but rather, the issuance of estimate assessments:

Aggressive Collection Does Not Mean Scam

Taxpayers should recognise that the current SARS enforcement environment differs materially from that of several years ago. Improved systems, enhanced automation, and broader access to third party financial data have strengthened SARS’ ability to pursue outstanding liabilities quickly and efficiently.

For taxpayers with unresolved debt, the head in the sand approach has become increasingly risky. Penalties and interest continue to accrue, whilst the risk of collection escalates. In enforcing recovery, SARS may issue third-party appointments to financial institutions, resulting in deductions of funds from taxpayer’s bank accounts, as well as personal liability for directors and trustees of non-compliant entities, and even civil and criminal action being taken.

Unfortunately, many taxpayers still delay engagement because they fear the financial implications of confronting their tax position. In practice, however, avoidance often worsens the liability substantially, as opposed to a proactive and voluntary approach which engages with legal tax debt relief mechanisms to achieve compliance.

Tax Debt Relief Remains Available

Genuine SARS debt does not automatically mean financial collapse or immediate enforcement without recourse.

South African tax legislation provides various relief mechanisms for qualifying taxpayers, including deferred payment arrangements, compromise applications, and the remission of penalties in appropriate circumstances.

Where taxpayers are experiencing genuine financial distress, properly structured compromise applications may allow for the writing-off of interest and penalties, and settlement of the capital tax liability due to SARS. Where this in not applicable, a deferral of payment arrangement with SARS remains available, allowing a taxpayer to settle their liability in an affordable and structured manner.

Taxpayers who are proactive and seek professional assistance early generally retain significantly more strategic options than those who wait until enforcement action has escalated.

Be Smarter Than the Scammer!

The rise of fake SARS settlement notifications reflects more than an increase in cybercrime. It reflects a tax environment where enforcement activity is intensifying, taxpayer anxiety is growing, and scammers are exploiting both as aggressively as they can.

Taxpayers should therefore adopt two critical principles with the first being to independently verify every SARS communication before making any payment or disclosing sensitive information, and the second being where a genuine tax debt exists, to address it proactively and professionally before SARS enforcement escalates further.

In the current tax environment, panic is expensive, but continued inaction is often far worse.

")