Individual taxpayers, companies, and trusts alike have been receiving urgent correspondence. This includes Final Letters of Demand to submit outstanding tax returns or risking possible criminal prosecution, as well as notices to trusts warning of imminent civil judgment if outstanding tax debts are not settled or payment arrangements not made.

SARS Is Landing Increasingly Hard Punches in Collecting Taxes Due

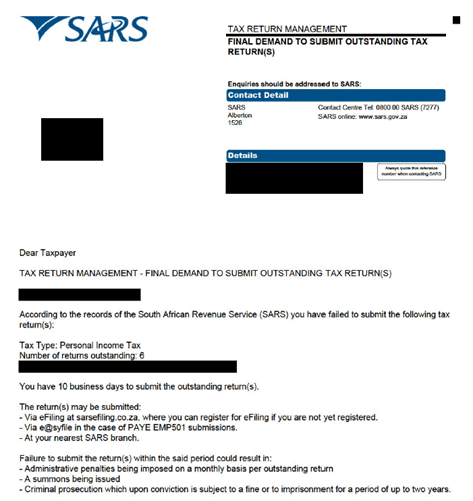

André Daniels, Head of Tax Controversy and Dispute Resolution at Tax Consulting South Africa, highlights a recent case where an individual taxpayer received a final demand to submit outstanding tax returns spanning six years, with SARS allowing the taxpayer only 10 business days to comply.

As shown in the excerpt below, SARS’ Tax Return Management warned that failure to do so could result in monthly administrative penalties per outstanding return, the issuing of a summons, and potential criminal prosecution. Upon conviction, this could lead to a fine or imprisonment of up to two years.

According to Daniels, such an aggressive approach against individual taxpayers is not commonly seen in practice, especially regarding outstanding tax returns. However, the extent of the non-compliance, being multiple years of outstanding personal income tax returns, likely prompted decisive intervention by the tax authority.

“Filing six historical tax returns within 10 business days is no easy task. This serves as a warning to taxpayers to remain compliant and up to date, and to act urgently to correct any non-compliance. When SARS comes to your door first, the options available to the taxpayer become far more limited.”

It is important to note that tax liabilities can escalate even in the absence of active communication from SARS. Many taxpayers only become aware of the full extent of their debt once recovery actions are already underway.

Daniels says in this instance, the taxpayer was unaware of outstanding returns, probably due to failure to check his eFiling profile regularly. All the while penalties and interest had been accumulating automatically.

Considering projected 2026/27 revenue exceeding R2.12 trillion, SARS is expected to further tighten its compliance efforts.

Stricter Enforcement Stretches Further

This firmer stance aligns with recent cases where SARS warned trusts of imminent civil judgment should they fail to settle outstanding tax debt or enter a payment arrangement within as little as 2 working days.

Daniels explains that this reflects SARS’ expectation of swift action to avoid stringent collection measures.

He reiterates that these types of notices carry significant legal weight and should not be underestimated. Taxpayers should respond promptly to all SARS correspondence regarding outstanding debt and make full use of grace periods or remedial options the tax authority provides.

SARS has consistently emphasised the importance of compliance among trusts, requiring that all tax returns and outstanding liabilities are up to date. This move toward filing civil judgments to recover tax debt marks a significant turning point that trusts and trustees should treat with urgency.

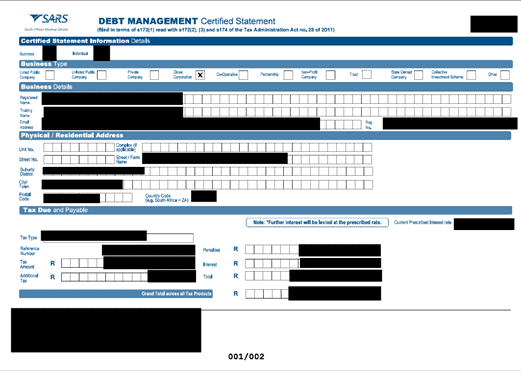

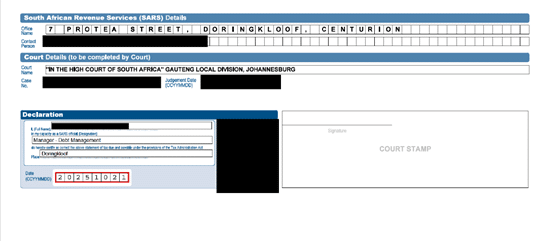

“When you reach this stage, SARS only needs to provide the court with a debt management certified statement of taxes due and payable, including interest and penalties. The registrar or clerk of the court can rubber-stamp the statement, giving it the effect of a civil judgment issued by the relevant court,” notes Daniels.

This is an example of what SARS takes to court to obtain a civil judgment:

Legal Basis for SARS’ Civil Judgment Powers

The assertive approach is firmly grounded in the powers granted to SARS in the Tax Administration Act (TAA), Part B of Chapter 11 dealing with the judgment process:

“If a person has an outstanding tax debt, SARS may, after giving the person at least 10 days’ notice, file with the clerk or registrar of a competent court a certified statement setting out the amount of tax payable and certified by SARS as correct.”

The Act also provides that SARS is not required to give prior notice if doing so would prejudice tax collection. Further to this, a certified statement filed under section 172 must be treated as a civil judgment lawfully given in the relevant court.

Dealing Decisively with Tax Debt

With the undisputed tax debt book currently exceeding R500 billion, SARS is increasingly using artificial intelligence (AI) and advanced data science as part of its digital transformation strategy, known as SARS Modernisation 3.0.

The initiative aims to eradicate tax non-compliance through sophisticated data analytics, refined algorithms and a shift from rules-based to behaviour-based risk management. Central to this vision is a move toward a system where “tax just happens,” as outlined in SARS’ Strategic Plan 2025/26–2029/30.

Within the framework of SARS’ legal mandate, this signals a future of faster, more efficient, and more proactive tax debt collection, particularly where debts are undisputed and therefore legally recoverable.

It is clear that all taxpayers — individuals, companies, and trusts —must ensure that their tax affairs are in order, up to date and that they respond promptly to any SARS correspondence.