After years of signalling a tougher stance on trust compliance, that moment has now arrived. The system is live, automated, and importantly, includes recurring monthly penalties.

The rollout of administrative penalties for the non-submission of trust tax returns marks a clear and deliberate follow-through on SARS’s stated enforcement agenda.

This is not a policy shift, but execution.

From Warning to Action

Many practitioners heard SARS’ warnings over the years, noted the tightening administrative framework, and — if we are honest — quietly wondered when enforcement would truly bite.

The groundwork was laid early in 2026 when SARS issued final demand notices to trusts with outstanding returns for the 2024 and 2025 years of assessment. These notices were formal triggers in terms of the Tax Administration Act (TAA), giving trustees a defined window to regularise their affairs.

The message was unmistakable: comply now, or face consequences.

That warning transitioned into formal enforcement when SARS published a notice in March 2026 categorising the non-submission of trust tax returns as an act of non-compliance subject to administrative penalties. The legal mechanism has long existed under sections 210 and 211 of the TAA. What changed is that trusts are now firmly within its crosshairs.

The 4 May 2026 Line in the Sand

Following industry feedback, largely centred on the complexity of trust administration, SARS granted a short reprieve. As a final grace period, the implementation of penalties was deferred to 4 May 2026.

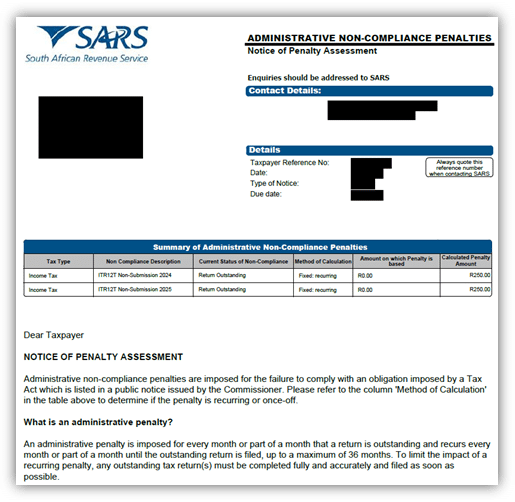

From the 5th of May, SARS began issuing penalty assessment notices (AP34) as the final deadline passed.

The Escalating Cost of Non-Compliance

The penalty regime is deliberately structured to escalate pressure. Fixed monthly penalties apply, ranging from R250 to R16,000 per outstanding return, depending on the trust’s taxable position.

What trustees must not misunderstand is that this is not a once-off penalty – it is imposed monthly until compliance is achieved and may be levied for up to 36 months.

In other words, procrastination compounds liability.

Even more significant is the issue of personal exposure. Trustees, as representative taxpayers, may be held personally liable where their failure results in penalties being imposed on the trust. That is a shift from a technical compliance issue to a governance risk.

No More “Dormant Trust” Excuse

One of the long-standing misconceptions in the trust space is that dormant or inactive trusts fall outside the compliance net. SARS has now explicitly dismantled that notion.

All trusts – active, dormant, or passive without assets – are required to register and submit annual income tax returns. There is no de minimis threshold, no inactivity exemption, and no tolerance for administrative neglect.

This is consistent with SARS’s broader compliance philosophy that if a taxpayer exists on the register, it must meet its statutory obligations or be formally deregistered.

A Broader Enforcement Strategy

These penalties do not exist in isolation. They form part of a broader, coordinated compliance drive targeting trusts. Over the past few years, SARS has introduced IT3(t) reporting, beneficial ownership disclosure requirements, and enhanced third-party data matching.

The administrative penalty regime is the enforcement backbone that makes these systems effective.

SARS has also made it clear that compliance is not optional. Its approach is increasingly data-driven, automated, and relentless. Once a trust is flagged as non-compliant, the process, from final demand to penalty imposition, is systematic and difficult to reverse.

What Trustees Need to Do Now

For trustees and their advisors, the implications are immediate:

- Outstanding returns must be submitted without delay, regardless of whether penalties have already been imposed.

- Dormant or inactive trusts must either comply or be formally deregistered with SARS.

- Internal governance processes must be strengthened to ensure ongoing compliance.

- Penalty remission may be requested, but it is not guaranteed – and it does not stop penalties from accruing in the interim.

Put bluntly: hoping SARS will not notice is no longer a strategy.

Conclusion: SARS Means What It Says

The enforcement of administrative penalties for trust non-compliance is not surprising. It is the predictable outcome of a revenue authority that has repeatedly committed to tightening compliance in the trust environment.

What is noteworthy is not the policy, but the follow-through.

SARS has demonstrated that its warnings are not rhetorical. When it signals enforcement, it delivers. And in the case of trusts, the era of passive non-compliance has officially ended.

The message to trustees is simple: comply, deregister, or pay.