TABLE OF CONTENTS

BUDGET HIGHLIGHTS

TAX REVENUE 2020/2021

GENERAL COMMENTARY

Taxpayers received a welcome message of support from Finance Minister, Tito Mboweni, in delivering his 2021 Budget Speech. In adopting a focus on economic recovery, following an unprecedented year of job losses, the Minister has for a second consecutive year afforded some relief to taxpayers with an above-inflation increase in the personal income tax brackets and rebates.

Despite the standing budget deficit, the Minister decided not to increase tax rates and has also withdrawn the decision communicated in the Medium-Term Budget Policy Statement to levy tax increases totalling R40 billion over the next four years.

Whilst the aim was not to drum up additional revenue with new tax policies, the Budget nonetheless delivered some interesting insights from a tax perspective. Most interesting, and in fulfilment of a promise made in the 2020 Budget Speech, National Treasury has proposed to reduce the corporate tax rate by 1% (one percent), with the new rate of 27% applicable from 1 April 2022. This decision was taken with a hope of further broadening the tax base and increasing South Africa’s attractiveness as an investment destination, as well as to reduce base erosion and profit shifting.

The Minister also made some interesting announcements regarding the taxation of wealthy persons and the introduction of future wealth taxes. SARS will establish a dedicated unit to investigate the compliance of wealthy individuals, with a focus on those individuals with complex financial arrangements. At the same time, Government will begin consolidating wealth data for taxpayers sourced through third-party information to further assess the feasibility of a wealth tax.

Other noteworthy changes include a proposed increase in the UIF contribution ceiling to R17,711.58 (which is open for public comment until 31 March) and excise or “sin” taxes to be increased by 8%, in another blow to the alcohol and tobacco industries following the prohibitions of related products as a result of the Covid-19 lockdown restrictions. The negative impact here, however, is a likely increase in the purchase of illicit tobacco and alcohol products, meaning additional revenue losses.

Thomas Lobban

Legal Manager and

General Tax Practitioner (SA)

INDIVIDUAL TAX

TAX RATES AND REBATES

Individuals, Estates & Special Trusts

Year ending 28 February 2022

| Taxable Income | Rate of tax (R) |

|---|---|

| R1 – R216 200 | 18% of taxable income |

| R216 201 – R337 800 | R38 916 + 26% of taxable income above R216 200 |

| R337 801 – R467 500 | R70 532 + 31% of taxable income above R337 800 |

| R467 501 – R613 600 | R110 739 + 36% of taxable income above R467 500 |

| R613 601 – R782 200 | R163 335 + 39% of taxable income above R613 600 |

| R782 201 – R1 656 600 | R229 089 + 41% of taxable income above R782 200 |

| R1 656 601 and above | R587 593 + 45% of taxable income above R1 656 600 |

Year ending 28 February 2021

| Taxable Income | Rate of tax (R) |

|---|---|

| R0 – R205 900 | 18% of taxable income |

| R205 901 – R321 600 | R37 062 + 26% of taxable income above R205 900 |

| R321 601 – R445 100 | R67 144 + 31% of taxable income above R321 600 |

| R445 101 – R584 200 | R105 429 + 36% of taxable income above R445 100 |

| R584 201 – R744 800 | R155 505 + 39% of taxable income above R584 200 |

| R744 801 – R1 577 300 | R218 139 + 41% of taxable income above R744 800 |

| R1 577 301 and above | R559 464 + 45% of taxable income above R1 577 300 |

| Rebates | 2021/2022 | 2020/2021 |

|---|---|---|

| Primary | R15 714 | R14 958 |

| Secondary (Persons 65 and older) | R8 613 | R8 199 |

| Tertiary (Persons 75 and older) | R2 871 | R2 736 |

| Age | Tax threshold | |

| Below age 65 | R87 300 | R83 100 |

| Age 65 to below 75 | R135 150 | R128 650 |

| Age 75 and older | R151 100 | R143 850 |

MEDICAL TAX CREDIT RATES

| Per month (R) | 2021/2022 | 2020/2021 |

|---|---|---|

| For the taxpayer who paid the medical scheme contributions | R332 | R319 |

| For the first dependant | R332 | R319 |

| For each additional dependant(s) | R224 | R215 |

TAKE-HOME PAY

The table below sets out a comparison of the take-home pay that an individual can expect based on the 2021 and 2022 tax tables:

| Take-home pay | |||||||

|---|---|---|---|---|---|---|---|

| 2021/2022 | 2021/2022 | 2021/2022 | 2020/2021 | 2020/2021 | 2020/2021 | ||

| Monthly gross | Annual equivalent | Under 65 | 65 – 74 | Over 75 | Under 65 | 65 – 74 | Over 75 |

| R7 275,00 | R87 300,00 | R7 275,00 | R7 275,00 | R7 275,00 | R7 212,00 | R7 275,00 | R7 275,00 |

| R10 000,00 | R120 000,00 | R9 509,50 | R10 000,00 | R10 000,00 | R9 446,50 | R10 000,00 | R10 000,00 |

| R15 000,00 | R180 000,00 | R13 609,50 | R14 327,25 | R14 566,50 | R13 546,50 | R14 229,75 | R14 457,75 |

| R20 000,00 | R240 000,00 | R17 550,83 | R18 268,58 | R18 507,83 | R17 419,17 | R18 102,42 | R18 330,42 |

| R30 000,00 | R360 000,00 | R24 858,33 | R25 576,08 | R25 815,33 | R24 659,17 | R25 342,42 | R25 570,42 |

| R40 000,00 | R480 000,00 | R31 706,25 | R32 424,00 | R32 663,25 | R31 413,75 | R32 097,00 | R32 325,00 |

| R50 000,00 | R600 000,00 | R38 106,25 | R38 824,00 | R39 063,25 | R37 774,25 | R38 457,50 | R38 685,50 |

| R80 000,00 | R960 000,00 | R56 143,92 | R56 861,67 | R57 100,92 | R55 715,58 | R56 398,83 | R56 626,83 |

| R110 000,00 | R1 320 000,00 | R73 843,92 | R74 561,67 | R74 800,92 | R73 415,58 | R74 098,83 | R74 326,83 |

| R130 000,00 | R1 560 000,00 | R85 643,92 | R86 361,67 | R86 600,92 | R85 215,58 | R85 898,83 | R86 126,83 |

| R150 000,00 | R1 800 000,00 | R96 965,92 | R97 683,67 | R97 922,92 | R96 273,25 | R96 956,50 | R97 184,50 |

The table below sets out a comparison of the PAYE that would have been/will be deducted from an individual’s salary in 2020 and 2021:

| PAYE to be deducted | |||||||

|---|---|---|---|---|---|---|---|

| 2021/2022 | 2021/2022 | 2021/2022 | 2020/2021 | 2020/2021 | 2020/2021 | ||

| Monthly gross | Annual equivalent | Under 65 | 65 – 74 | Over 75 | Under 65 | 65 – 74 | Over 75 |

| R7 275,00 | R87 300,00 | – | – | – | R63,00 | – | – |

| R10 000,00 | R120 000,00 | R490,50 | – | – | R553,50 | – | – |

| R15 000,00 | R180 000,00 | R1 390,50 | R672.75 | R433.50 | R1 453,50 | R770,25 | R542,25 |

| R20 000,00 | R240 000,00 | R2 449,17 | R1 731,42 | R1,492.17 | R2 580,83 | R1 897,58 | R1 669,58 |

| R30 000,00 | R360 000,00 | R5 141,67 | R4 423,92 | R4,184.67 | R5 340,83 | R4 657,58 | R4 429,58 |

| R40 000,00 | R480 000,00 | R8 293,75 | R7 576,00 | R7,336.75 | R8 586,25 | R7 903,00 | R7 675,00 |

| R50 000,00 | R600 000,00 | R11 893,75 | R11 176,00 | R10,936.75 | R12 225,75 | R11 542,50 | R11 314,50 |

| R80 000,00 | R960 000,00 | R23 856,08 | R23 138,33 | R22,899.08 | R24 284,42 | R23 601,17 | R23 373,17 |

| R110 000,00 | R1 320 000,00 | R36 156,08 | R35 438,33 | R35,199.08 | R36 584,42 | R35 901,17 | R35 673,17 |

| R130 000,00 | R1 560 000,00 | R44 356,08 | R43 638,33 | R43,399.08 | R44 784,42 | R44 101,17 | R43 873,17 |

| R150 000,00 | R1 800 000,00 | R53 034,08 | R52 316,33 | R52,077.08 | R53 726,75 | R53 043,50 | R52 815,50 |

INTEREST EXEMPTION

| South African Sourced Interest | |

|---|---|

| Persons under 65 years | R23 800 |

| Persons 65 years and older | R34 500 |

South African sourced interest income earned by non-residents is exempt if the non-resident was absent from the country for an aggregate of 183 days in the 12 months preceding the accrual of that interest.

TAX-FREE INVESTMENTS

Amounts received by or accrued to an individual in respect of particular prescribed investment instruments and policies are exempt. Contributions to these prescribed investments/policies are subject to an annual limit of R36 000. Currently, a R500 000 lifetime limit applies.

DIVIDENDS

Dividends received by individuals from South African companies are generally exempt from income tax, but dividends tax at a rate of 20% is withheld by the entities paying the dividends to the individuals.

FOREIGN DIVIDENDS

Most foreign dividends received by individuals from foreign companies (shareholding of less than 10% in the foreign company) are taxable at a maximum effective rate of 20%. No deductions are allowed for expenditure to produce foreign dividends.

FOREIGN INTEREST

Foreign interest received by or accrued to a resident is subject to normal tax in South Africa.

TRAVEL EXPENSES

Rates per kilometre, which may be used in determining the allowable deduction for business travel against an allowance or advance where actual costs are not claimed, are determined by using the table on the SARS website www.sars.gov.za.

- If the travel allowance is applicable to a portion of the tax year, the fixed cost is reduced proportionately.

- Where the travel allowance is based on actual distance travelled by the employee for business purposes, no tax is payable on an allowance paid by an employer to an employee, up to the rate of R3,82 per kilometre regardless of the value of the vehicle or distance travelled. This alternative is not available if other compensation in the form of an allowance or reimbursement (other than for parking or toll fees) is received from the employer in respect of the vehicle.

- It is compulsory to keep a logbook of travels in order to claim business travel expenses.

- When claiming actual expenditure, the cost of the vehicle must be limited to the maximum allowed value as per the SARS website www.sars.gov.za for the purposes of calculating finance charges and wear and tear.

SUBSISTENCE ALLOWANCE

Where the recipient is obliged to spend at least one night away from his or her usual place of residence on business, and the accommodation to which that allowance or advance relates is in the Republic of South Africa, and the allowance or advance is granted to pay for meals and incidental costs or incidental costs only, an amount, published on the SARS website www.sars.gov.za, under Legal Counsel / Secondary Legislation / Income Tax Notices / 2021, is deemed to have been expended per day.

Where the accommodation to which that allowance or advance relates is outside the Republic of South Africa, a specific amount per country is deemed to have been expended. Details of these amounts are published on the SARS website under Legal Counsel / Secondary Legislation / Income Tax Notices / 2019.

Where the recipient is by reason of the duties of his or her office or employment obliged to spend a part of a day away from his or her usual place of work or employment, a reimbursement or advance for expenditure actually incurred by the recipient is exempt if the recipient is allowed by his or her principal to incur expenditure on meals and other incidental costs for that part of a day and the amount of the expenditure does not exceed an amount published on the SARS website www.sars.gov.za, under Legal Counsel / Secondary Legislation / Income Tax Notices / 2021.

TRAVELLING ALLOWANCE

Rates per kilometre, which may be used in determining the allowable deduction for business travel against an allowance or advance where actual costs are not claimed, are determined using the table published on the SARS website www.sars.gov.za, under Legal Counsel / Secondary Legislation / Income Tax Notices / Fixing of rate per kilometre in respect of motor vehicles.

Note:

- 80% of the travelling allowance must be included in the employee’s remuneration for the purposes of calculating PAYE. The percentage is reduced to 20% if the employer is satisfied that at least 80% of the use of the motor vehicle for the tax year will be for business purposes.

- No fuel cost may be claimed if the employee has not borne the full cost of fuel used in the vehicle, and no maintenance cost may be claimed if the employee has not borne the full cost of maintaining the vehicle (e.g. if the vehicle is covered by a maintenance plan)

- The fixed cost must be reduced on a pro-rata basis if the vehicle is used for business purposes for less than a full year

- The actual distance travelled during a tax year, and the distance travelled for business purposes substantiated by a log book, are used to determine the costs which may be claimed against a travelling allowance.

RETIREMENT FUND CONTRIBUTIONS

Contributions to a pension, provident or retirement annuity fund during a tax year are deductible by the member of the fund. The deduction is limited to the greater of:

- 27.5% of the employee’s remuneration for PAYE purposes (excluding retirement fund lump sums and severance benefits); or

- 27.5% of the employee’s taxable income (excluding retirement fund lump sums and severance benefits).

The deduction is limited to a maximum amount of R 350 000. If contributions exceed the limit during a particular tax year, the contributions are carried over to the next tax year.

DONATIONS

Deductions in respect of donations to certain public benefit organisations are limited to 10% of taxable income (excluding retirement fund lump sums and severance benefits). The amount of donations exceeding 10% of the taxable income is treated as a donation to qualifying public benefit organisations in the following tax year.

Donations tax is levied at a flat rate of 20% on the cumulative value of donations not exceeding R30 million and a rate of 25% on the cumulative value exceeding R30 million. This was effective March 2018. Donations made prior to this date must not be included in the cumulative total.

The first R100 000 of donations in each year by an individual is exempt from donations tax, as well as donations to spouses and certain public benefit organisations.

Donations made by non-residents are also exempt from donations tax.

LUMP SUM BENEFITS

Lump sum benefits in consequence of the withdrawal of membership of a retirement fund, including amounts assigned in terms of divorce settlements in certain circumstances, other than death/retirement lump sum benefits, are taxed according to the following table:

| Taxable income from withdrawal benefits | Tax payable |

|---|---|

| R1 – R25 000 | 0% of taxable income |

| R25 001 – R660 000 | 18% of taxable income above R25 000 |

| R660 001 – R990 000 | R114 300 + 27% of taxable income above R660 000 |

| R990 001 and above | R203 400 + 36% of taxable income above R990 000 |

Lump sum benefits in consequence of retirement/death are taxed according to the following table:

| Taxable income from retirement benefits | Tax payable |

|---|---|

| R1 – R500 000 | 0% of taxable income |

| R500 001 – R700 000 | 18% of taxable income above R500 000 |

| R700 001 – R1 050 000 | R36 000 + 27% of taxable income above R700 000 |

| R1 050 001 and above | R130 500 + 36% of taxable income above R1 050 000 |

* Taxable income is cumulative and includes all lump sum payments whether on retirement (after 1 October 2007) or withdrawal (after 1 March 2009), or a severance benefit (after 1 March 2011).

CAPITAL GAINS TAX (CGT)

As from 1 October 2001, Capital Gains Tax (CGT) applies to residents’ worldwide assets and to non-residents’ immovable property or assets of a permanent establishment situated in South Africa.

| Maximum effective rate of tax | |

|---|---|

| Individuals and special trusts | 18% |

| Companies | 22.4% |

| Other trusts | 36% |

| Inclusion rates | |

|---|---|

| Individuals, special trusts and individual policyholder funds | 40% |

| Companies and trusts | 80% |

| Exclusions | |

|---|---|

| Individuals, special trusts and individual policyholder funds | R40 000 |

| Individuals in year of death | R300 000 |

| Primary residence exclusion on the disposal of a primary residence | R2 million gain/loss |

| Small business assets (persons over age 55 and market value of assets not more than R10 million) | R1.8 million |

| CGT example | ||

|---|---|---|

| Salary | R180 000 | |

| Sale of primary residence | ||

| – Proceeds | R4 000 000 | |

| – Agent commission | (R200 000) | |

| – Purchase price | (R1 500 000) | |

| – Improvements | (R150 000) | |

| Sub total | R2 150 000 | |

| Primary residence exclusion | (R2 000 000) | |

| Gain from sale | R150 000 | |

| Sale of shares | ||

| – Proceeds | R50 000 | |

| – Purchase price | (R35 000) | |

| Gain from sale | R15 000 | |

| Total capital gains | R165 000 | |

| Less: Annual exclusion | (R40 000) | |

| Total | R125 000 | |

| Apply inclusion rate (40%) | R50 000 | |

| Total taxable income | R230 000 |

TRUSTS

TRUSTS TAX RATES

| Rate of tax | 2015 | 2016-2017 | 2018-2022 |

|---|---|---|---|

| All taxable income | 40% | 41% | 45% |

Special trusts are taxed at the rates applicable to individuals, but are not entitled to any rebate. The 40% inclusion rate for a taxable capital gain applies to both types of special trusts and 80% inclusion rate for normal trusts.

A special trust is one created:

- Solely for the benefit of a person affected by a mental illness or serious physical disability which prevents that person from earning sufficient income to maintain him/herself. Where the person for whose benefit the trust was established dies prior to or on the last day of the year of assessment the trust will no longer be regarded as a special trust;

- As a testamentary trust established solely for the benefit of minor children who are alive and related to the deceased on the date of death. Where the youngest beneficiary turns 18 years of age prior to or on the last day of the year of assessment, the trust will no longer be regarded as a special trust.

SECTION 7C

What is Section 7C?

Section 7C is an anti-avoidance provision designed to prevent avoidance of both donations tax and estate duty through low or no interest loans granted to trusts.

Implications of Section 7C?

SARS will deem the interest foregone, on a loan to a trust where the interest is less than the official interest rate, as a donation. This donation is deemed to be made on the last day of the year of assessment of the trust and will be subject to donations tax.

The lender must be either a connected natural person, or a company who granted the loan at the instance of that natural person. This applies to all loan account balances on or after 1 March 2017.

The provision does not apply to loans granted to a trust for the purchase of the lender’s or the spouse’s primary residence.

The official interest rate is linked to the repurchase rate plus 1% and is published on the SARS website. The most recent changes are as follows:

| Date from | Date to | Rate |

|---|---|---|

| 01.04.2016 | 31.07.2017 | 8.00% |

| 01.08.2017 | 31.03.2018 | 7.75% |

| 01.04.2018 | 30.11.2018 | 7.50% |

| 01.12.2018 | 31.07.2019 | 7.75% |

| 01.08.2019 | 31.01.2020 | 7.50% |

| 01.02.2020 | 31.03.2020 | 7.75% |

| 01.04.2020 | 30.04.2020 | 6.25% |

| 01.05.2020 | 30.05.2020 | 5.25% |

| 01.06.2020 | 31.07.2020 | 4.75% |

| 01.08.2020 | Until change in Repo rate | 4.50% |

Non-Residents:

Loans by non-residents are not subject to the effect of donations tax as a result of Section 7C since non-residents are exempt from donations tax. Loans from non-residents may nonetheless be subject to transfer pricing provisions.

Distributions to non-residents are fully taxable in the trust at the trust’s applicable tax rate.

COMPANIES

COMPANY TAX RATES

(Unless otherwise stated, financial years ending on any date between 1 April 2021 and 31 March 2022)

| Basic rate (other than entities specified below) | 28% |

| Companies in certain special economic zones | 15% |

Small Business Corporations (annual turnover of R20 million or less):

Financial years ending on any date between 1 April 2021 and 31 March 2022

| Taxable income | Rate of tax |

|---|---|

| R1 – R87 300 | 0% of taxable income |

| R87 301 – R365 000 | 7% of taxable income above R87 300 |

| R365 001 – R550 000 | 19 439 + 21% of taxable income above R365 000 |

| R550 001 and above | 58 289 + 28% of the amount above R550 000 |

Micro-business (elective presumptive turnover tax for qualifying annual turnover of R1 million or less)*:

Years of assessment commencing on 1 March 2021 or ending on 28 February 2022.

| Taxable turnover | Rate of tax |

|---|---|

| R1 – R335 000 | 0% of taxable turnover |

| R335 001 – R500 000 | 1% of taxable turnover above R335 000 |

| R500 001 – R750 000 | R1 650 + 2% of taxable turnover above R500 000 |

| R750 001 and above | R6 650 + 3% of taxable turnover above R750 000 |

DONATIONS

In the case of a taxpayer who is not an individual, exempt donations are limited to casual gifts not exceeding R10 000 per annum in total.

Donations between companies forming part of the same group of companies and donations to certain public benefit organisations are exempt from donations tax.

VAT

The VAT rate remained unchanged at 15%

Compulsory Registration

It is mandatory for a business to register for VAT if the total value of taxable supplies made in any consecutive twelve month period exceeded or is likely to exceed R1 million. The business must complete a VAT 101 – Application for Registration form and submit it to SARS within 21 days from date of exceeding R1 million.

Voluntary Registration

A business may also choose to register voluntarily for VAT if the value of taxable supplies made or to be made is less than R1 million, but has exceeded R50 000 in the past period of 12 months.

DIVIDENDS

Dividends are subject to dividends tax which is withheld from the gross dividend declared, before being paid to the beneficial owners. The entity declaring the dividend is liable for withholding the tax and paying it to SARS.

The following rates are applicable:

| Beneficial owner | Dividend withholding tax rate |

|---|---|

| Resident individuals | 20% |

| Resident companies | 0% |

| Non-resident individuals and companies | Refer to tax rates per South African DTA Agreements – available on the SARS website |

FRINGE BENEFITS

Employer-owned vehicles

- The taxable value is 3.5% of the determined value (the cash cost including VAT) of each vehicle per month. Where the vehicle is:

- the subject of a maintenance plan when the employer acquired the vehicle the taxable value is 3,25% of the determined value; or

- acquired by the employer under an operating lease, the taxable value is the cost incurred by the employer under the operating lease plus the cost of fuel.

- 80% of the fringe benefit must be included in the employee’s remuneration for the purposes of calculating PAYE. The percentage is reduced to 20% if the employer is satisfied that at least 80% of the use of the motor vehicle for the tax year will be for business purposes.

- On assessment, the fringe benefit for the tax year is reduced by the ratio of the distance travelled for business purposes, substantiated by a log book, divided by the actual distance travelled during the tax year.

- On assessment further relief is available for the cost of licence, insurance, maintenance and fuel for private travel, if the full cost thereof has been borne by the employee and if the distance travelled for private purposes is substantiated by a log book.

Interest-free or low-interest loans

The difference between interest charged at the official rate, and the actual amount of interest charged, is to be included in gross income.

Residential accommodation

- The value of the fringe benefit to be included in gross income is the lower of the benefit calculated by applying a prescribed formula, or the cost to the employer if the employer does not have full ownership of the accommodation.

- The formula will apply if the accommodation is owned by the employee, but it does not apply to holiday accommodation hired by the employer from non-associated institutions.

SECURITIES TRANSFER TAX

Securities transfer tax (STT) is payable upon the transfer of unlisted shares. This includes the buying back, redemption or cancellation of shares. STT is levied at 0.25% of the value of the shares transferred and is due within two months after the end of the month in which the shares were transferred.

TAX ON INTERNATIONAL AIR TRAVEL

R190 per passenger departing on international flights, excluding flights to Botswana, Lesotho, Namibia and eSwatini, in which case the tax is R100.

SKILLS DEVELOPMENT LEVY

A skills development levy is payable by employers at a rate of 1% of the total remuneration paid to employees. Employers paying annual remuneration of less than R500 000 are exempt from the payment of Skills Development Levies.

UNEMPLOYMENT INSURANCE CONTRIBUTIONS

- Unemployment insurance contributions are payable monthly by employers, on the basis of a contribution of 1% by employers and 1% by employees, based on the employees’ remuneration below a certain amount.

- Employers not registered for PAYE or SDL must pay the contributions to the Unemployment Insurance Commissioner.

- The proposed UIF ceiling limit increase is R17 711.58 per month.

- The effective date for the increase in the ceiling is not yet confirmed. The National Treasury published a draft public notice on 26 February 2021, which remains open for public comment until 31 March 2021. The effective date will only be confirmed upon publication of the final notice in the Government Gazette.

OTHER

PROVISIONAL TAX

A provisional taxpayer is any person who earns income by way of remuneration from an unregistered employer, or income that is not remuneration, or an allowance or advance payable by the person’s principal. An individual is not required to pay provisional tax if he or she does not carry on any business, and the individual’s taxable income:

- Will not exceed the tax threshold for the tax year; or

- From interest, dividends, foreign dividends, rental from letting of fixed property, and remuneration from an unregistered employer will be R30 000 or less for the tax year.

Provisional tax returns showing an estimation of total taxable income for the year of assessment are required from provisional taxpayers.

Deceased estates are not provisional taxpayers.

ESTATE DUTY

| Value of estate | Rate |

|---|---|

| R0 to R30 000 000 | 20% of the dutiable amount of a deceased estate |

| Exceeding R30 000 000 | 25% of the dutiable amount of a deceased estate |

Estate duty is levied on the dutiable amount of a deceased estate (property of residents and SA property of non-residents). Deductions include: a standard abatement of R3.5 million per estate (R7 million for a married couple) and certain other deductions, the most important of which is the deduction for property accruing to a surviving spouse.Estate duty is levied on the dutiable amount of a deceased estate (property of residents and SA property of non-residents). Deductions include: a standard abatement of R3.5 million per estate (R7 million for a married couple) and certain other deductions, the most important of which is the deduction for property accruing to a surviving spouse.

TRANSFER DUTY

Paid on acquisition of immovable property where the transaction is not subject to VAT. Transfer duty is also payable on the acquisition of residential property through an interest in a company or trust. The rates of duty are as follows:

Years of assessment commencing on 1 March 2021 or ending on 28 February 2022.

| Value of property | Rate |

|---|---|

| R1 – R1 000 000 | 0% |

| R1 000 001 – R1 375 000 | 3% of the value above R1 000 000 |

| R1 375 001 – R1 925 000 | R11 250 + 6% of the value above R 1 375 000 |

| R1 925 001 – R2 475 000 | R44 250 + 8% of the value above R 1 925 000 |

| R2 475 001 – R11 000 000 | R88 250 +11% of the value above R2 475 000 |

| R11 000 001 and above | R1 026 000 + 13% of the value exceeding R11 000 000 |

WITHHOLDING TAXES

| Other payments to non-residents | |

|---|---|

| Royalties | 15% |

| Interest | 15% |

| Sportsmen and entertainers who perform in SA | 15% |

| Fixed property acquired in SA from a seller that is a non-resident: | |

| If the non-resident is a natural person | 7.5% |

| If the non-resident is a company | 10% |

| If the non-resident is a trust | 15% |

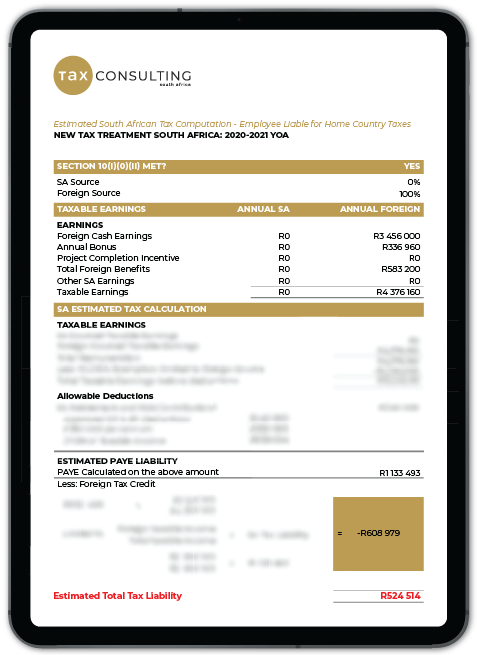

EXPATRIATE TAX

FOREIGN REMUNERATION EXEMPTION

Foreign remuneration has experienced quite a lot of attention in the past 4 years. What was originally a full exemption under Section 10(1)(o)(ii), was limited to R1.25 million from 1 March 2020 following Tito Mboweni’s 2020 Budget Speech. This comes after the initial amendment which was promulgated in December 2017 that capped the exemption at R1 million. These changes have caused numerous South African tax residents abroad to cut ties with the country.

Although it appears that this may bring relief to South African tax residents abroad, the additional R250 000 is mainly wiped out by the effect of the weakening Rand and fringe benefits which will inflate their total package.

Government has proposed to phase in a new exchange control treatment as from 1 March 2021 which is also aimed at reducing the increasing emigration rates. We will see a new verification process with regards to remuneration earned abroad and offshore transfers which allows identical treatment of natural person emigrants and natural person residents.

LEXISNEXIS EXPATRIATE TAX TEXTBOOK

PROFESSIONAL PARTNER NETWORK

THE PREFERRED NETWORK FOR FELLOW PROFESSIONALS IN LAW, ACCOUNTING, AND TAX

Increasingly complicated and ever-changing tax legislation means that every industry requires a professional partner capable of providing innovation tax consulting solutions while keeping you in the know of latest industry developments.

It is inevitable that your clients will require advice on matters of taxation at some stage, be it with a dispute, a commercial transaction or general tax compliance. We appreciate the risk of taking on matters that fall outside your firm’s field of expertise, especially where your client may suffer adverse tax consequences.

Our diverse international network allows us to harness resources from around the world, empowering us to set the trends and create a benchmark in our industry.

Professionals are confidently servicing their clientele through us, under the umbrella of their own firm, thereby expanding their client base and service offerings.

To be a part of our network, means to be a step above the rest, at the forefront of innovation and driven by a competitive edge.